In this method, you calculate lifo periodic vs perpetual an average for the period instead of moving transactions over when the company bought or sold something during the period. Periodic inventory is an accounting stock valuation practice that’s performed at specified intervals. Businesses physically count their products at the end of the.

Lifo valuation considers the last items in inventory are sold first, as opposed to lifo, which considers the first inventory items being sold first. If you want to use lifo, you must elect this. See the example lifo perpetual inventory card below to get an idea of how it works.

The retail sales for this product in this company were $25,000 from jan. 1, 2019 to jan. From the perpetual lifo inventory card above, you can calculate the cost of ending inventory as the total cost balance from the last row, or $7,200.

We go through a thorough e. Therefore, the value of ending inventory under both systems will. Learn how to calculate cost of merchandise sold and cost of ending inventory using the perpetual lifo method of inventory valuation.

The perpetual inventory system requires a lot more setup, but once it's in place, it's much easier to operate. Every piece of inventory you own is entered into your computer system as it's purchased. The basic concept underlying perpetual lifo is the last in, first out (lifo) cost layering system.

Under lifo, you assume that the last item entering inventory is the first one to be used. For example, consider stocking the shelves in a food store, where a customer purchases the item in front, which was likely to be the last item added to the. When it comes to the fifo method, mike needs to utilize the older costs of acquiring his inventory and work ahead from there.

So, mike’s cogs calculation is as follows: 200 units x $800 = $160,000. 300 units x $825 = $247,500.

200 units x $850 = $170,000. 300 units x $875 = $262,500. 100 units x $900 = $90,000.

Cost of goods sold (cogs): $560 + $336 + $168 + $436 = $1,500. [$240 + $84] = $324.

When lifo method is used in a perpetual inventory system, it is typically known as “lifo perpetual system”. The above example explains the use of lifo perpetual system in a merchandising company. In manufacturing companies, it is used.

We can calculate this by applying the lifo method used in cfi’s lifo calculator. Following the schedule above, we can calculate the cost of the remaining pills and the cost of goods sold. 100 pills sold at $2. 25/pill = $225 in cogs.

100 pills sold at $1. 65/pill = $165 in cogs. How to use the fifo lifo calculator? Follow these steps to use the fifo lifo calculator.

Type the total units solved in the textbox. Click calculate fifo or calculate lifo according to your need. Add more fields if needed.

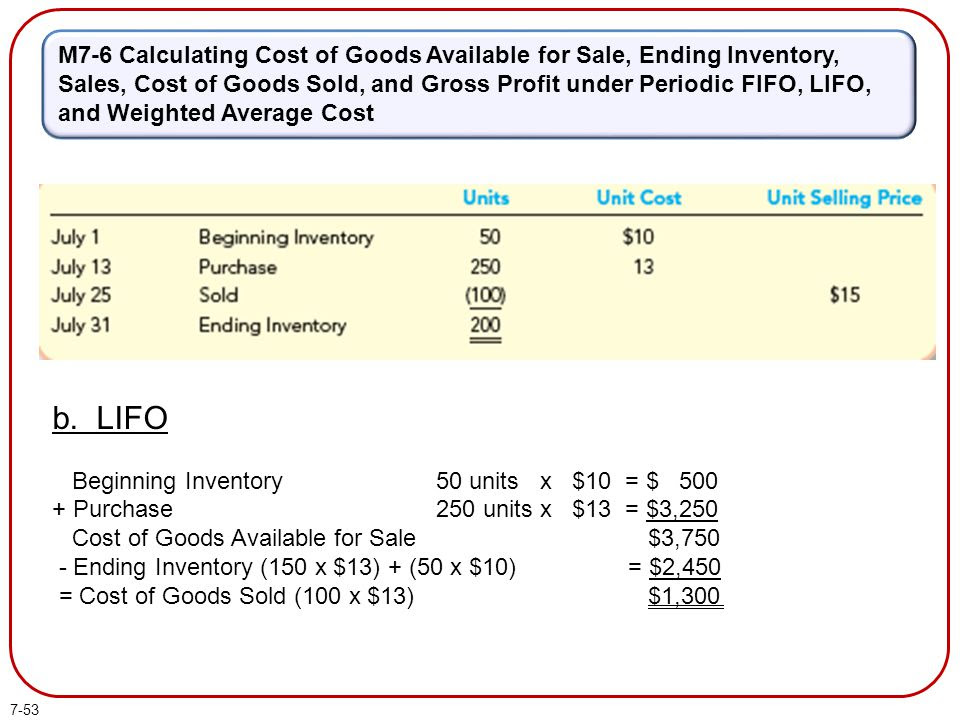

In this formula, your beginning inventory is the dollar amount of product the company has at the onset of the accounting period. The net purchases portion of this formula is the cost of any new product or inventory items bought during the accounting period.