Capm beta calculation in excel. Levered beta measures the risk of a firm with debt and equity in its capital structure to the volatility of the market. The other type of beta is known as unlevered beta. unlevering the beta removes any beneficial or detrimental effects gained by adding debt to the firm's capital structure.

Is levered or unlevered beta used in capm? After unlevering the betas, we can now use the appropriate “industry” beta (e. g. The mean of the comps' unlevered betas) and relever it for the appropriate capital structure of the company being valued.

After relevering, we can use the levered beta in the capm formula to calculate cost of equity. Is levered or unlevered beta used in capm? After unlevering the betas, we can now use the appropriate “industry” beta (e. g.

The mean of the comps' unlevered betas) and relever it for the appropriate capital structure of the company being valued. After relevering, we can use the levered beta in the capm formula to calculate cost of equity. Which beta is used in capm?

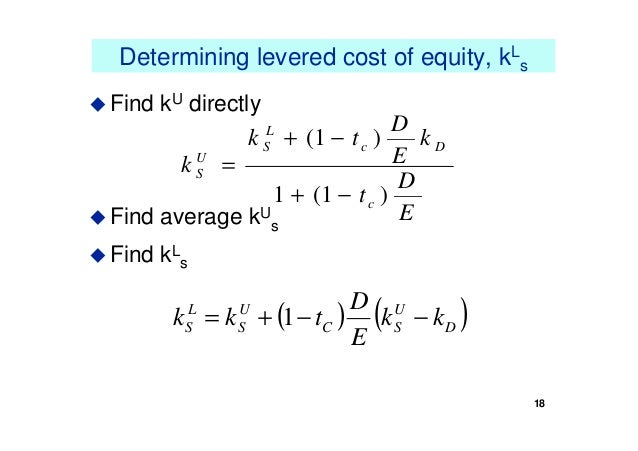

Levered beta or equity beta is the beta that contains the effect. I have derived a firm's cost of equity using the wacc formula (see here), which means that the cost of equity has factored in the firms' debt (i. e. Levered beta) and now i need to calculate the firm's unlevered beta.

Here is my solution thus far, please let me know if i am on the right track. Formula to calculate unlevered beta: Is capm beta levered or unlevered?

Levered beta or equity beta is the beta that contains the effect of capital structure i. e. Debt and equity both. The beta that we calculated above is the levered beta.

Both unlevered beta and levered beta measure the volatility of a inventory in relation to movements in the overall market. It is used in capm to find bea’s cost of equity. To determine bea’s cost of equity, the analyst must first calculate the unlevered beta (or asset beta).

Then, the analyst should round up the wacc to two decimal places. Levered beta measures the risk of a firm with debt and equity in its capital structure to the volatility of the market. The other type of beta is known as unlevered beta. unlevering the beta removes any beneficial or detrimental effects gained by adding debt to the firm's capital structure.

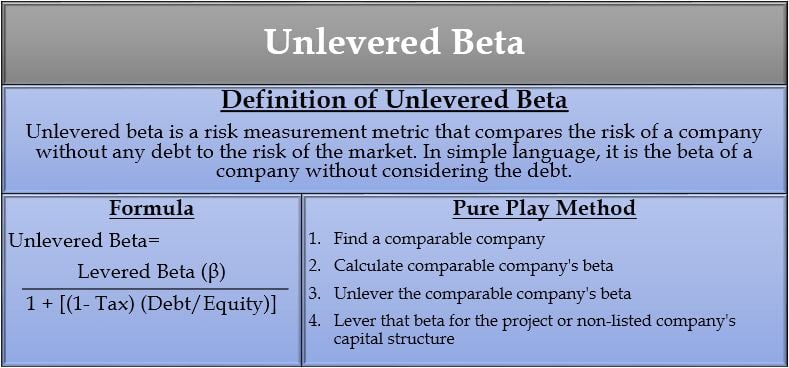

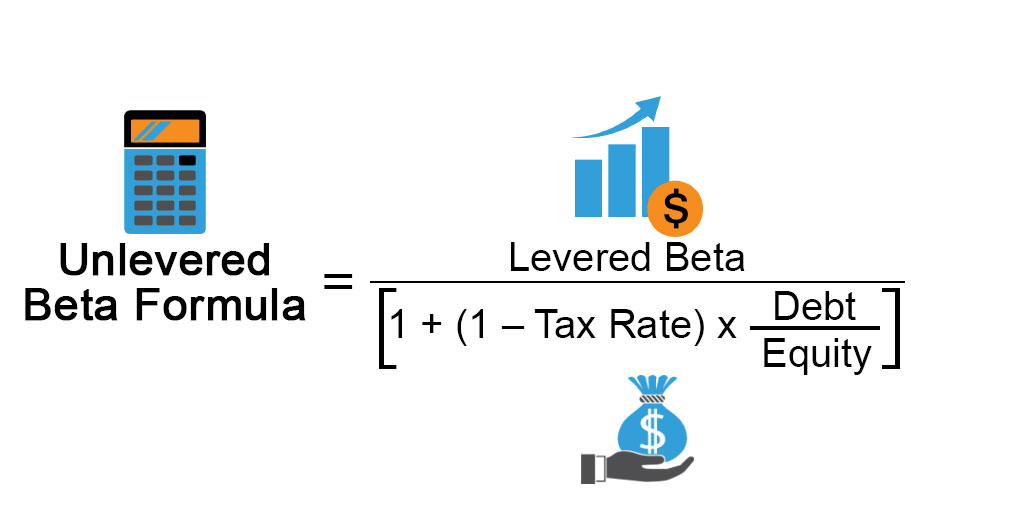

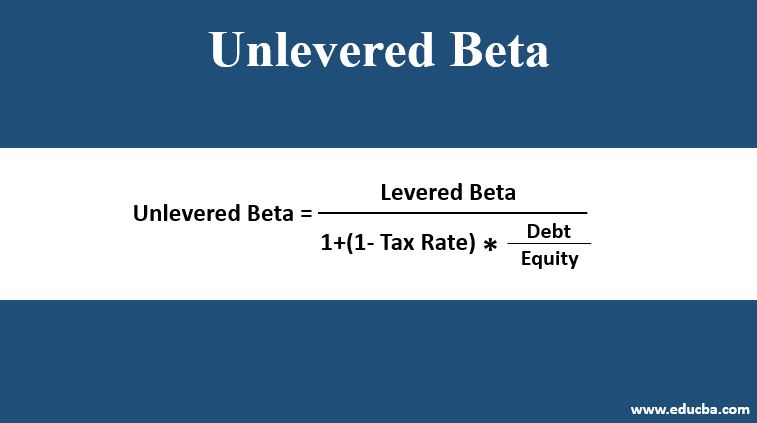

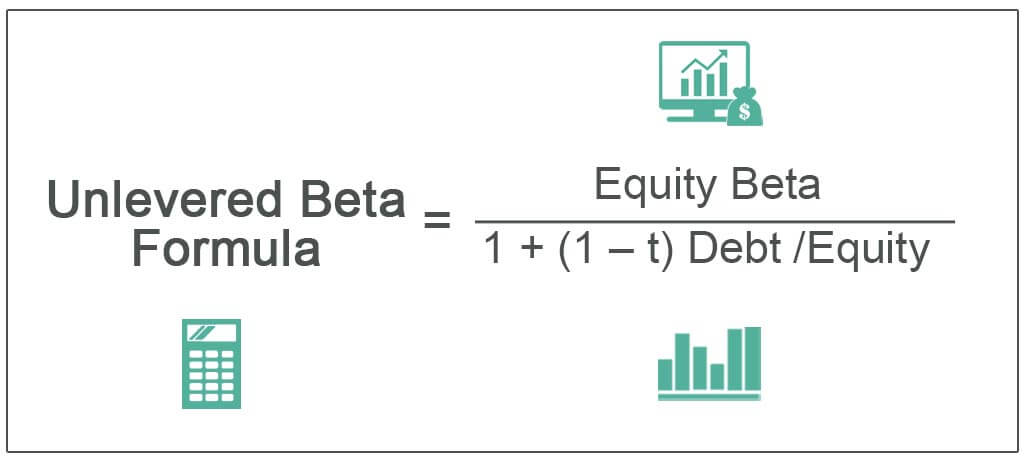

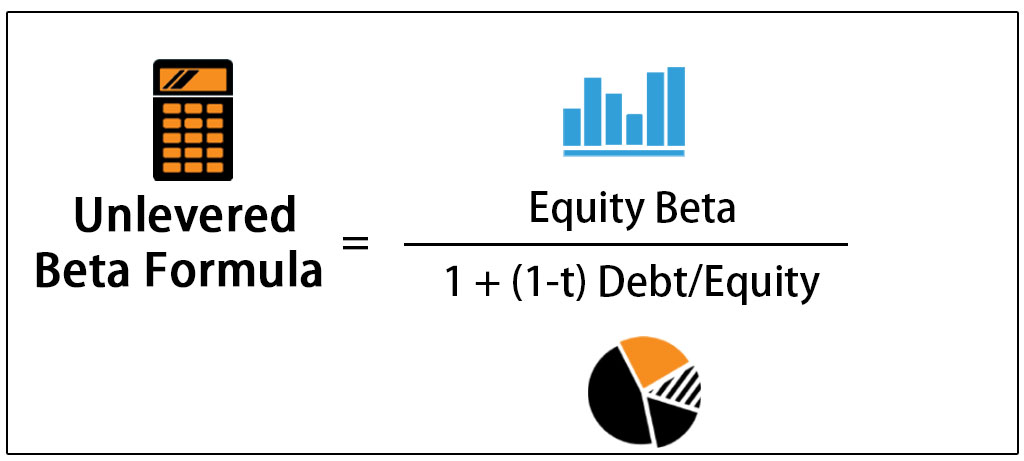

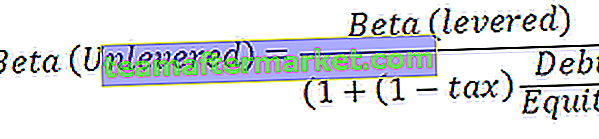

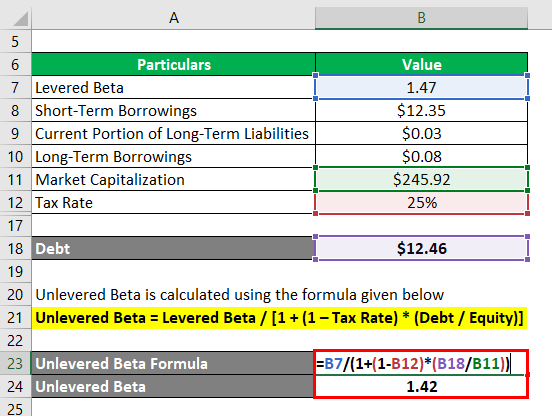

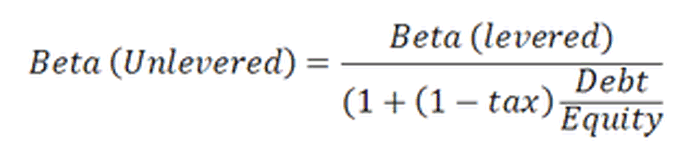

The unlevered beta of a company is its probability of bankruptcy, given the overall market risk. The formula for calculating the unlevered beta is: What is unlevered beta formula?

Advertisement after unlevering the betas, we can now use the appropriate “industry” beta (e. g. The mean of the comps’ unlevered betas) and relever it for the appropriate capital structure of the company being valued. After relevering, we can use the levered beta in the capm formula to calculate cost ofread more →

Levered beta or equity beta is the beta that contains the effect of capital structure i. e. Debt and equity both. The beta that we calculated above is the levered beta.

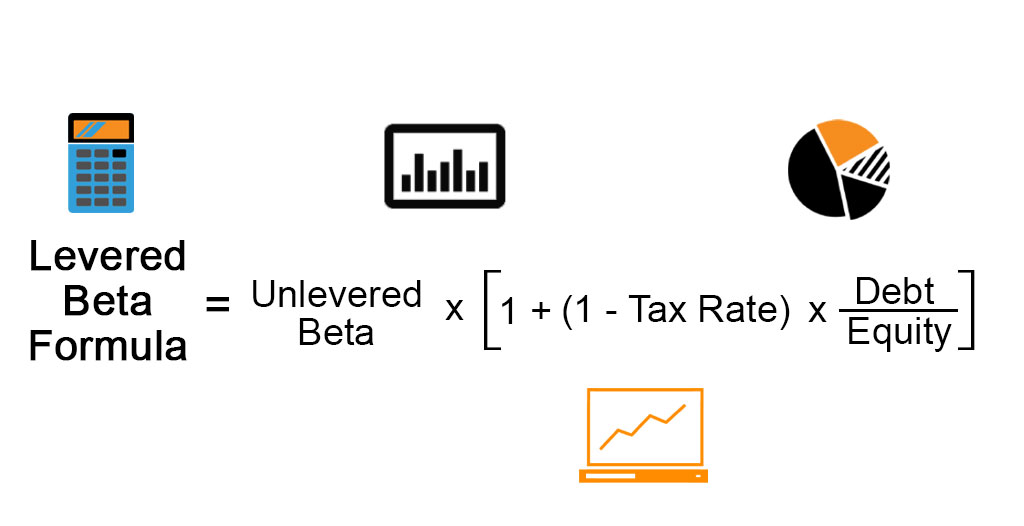

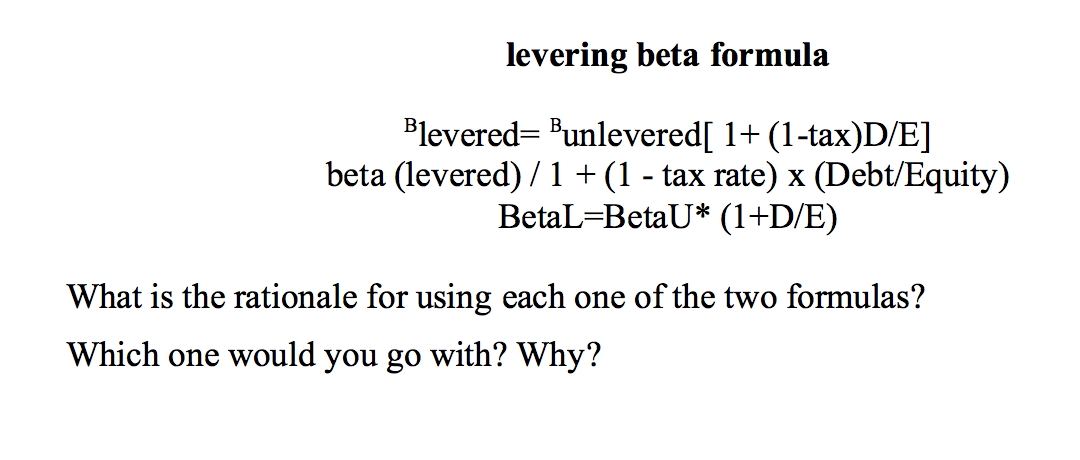

How do you calculate levered beta in capm? Levered beta = unlevered beta * (1+d/e), where d/e =. Unlevered beta shows the volatility of returns without financial leverage.

Unlevered beta is known as asset beta, while the levered beta is. An integral component of the capital asset pricing model ( capm ), beta quantifies the relationship between systematic risk and the expected return. Moreover, there are two distinct types of beta measured in corporate finance:

Levered beta → inclusive of capital structure (d/e) effects. Unlevered beta → removed capital structure (d/e) effects. Formula for unlevered beta.

Unlevered beta or asset beta can be found by removing the debt effect from the levered beta. Dividing levered beta with this debt effect will give you unlevered beta. Beta is used in the capital asset pricing model (capm), which describes the relationship between systematic risk and expected return for assets (usually stocks).

Is beta levered or unlevered? Levered beta (commonly referred to as just beta or equity beta) is a measure of market risk.